Growth in PET and PET/CT procedure volume in the U.S. slowed to a single-digit rate in 2008 compared to 2007, as opposed to the double-digit annual growth rates the modality enjoyed before 2007, according to a new study published by market research firm IMV Medical Information Division of Des Plaines, IL.

The total number of PET and PET/CT patient studies conducted in the U.S. stood at 1.52 million in 2008, representing growth of only 4% above the 1.48 million procedures performed in 2007. That compares to an average annual growth rate of 10.4% from 2005 to 2008, according to the IMV survey of more than 2,000 sites with fixed and mobile PET and PET/CT units. There were 1.13 million studies performed in 2005.

"Several factors may have contributed to this slowdown in both PET procedures and market growth of the market for PET purchases over the next few years," said Lorna Young, IMV's senior director of market research. "These factors include the Deficit Reduction Act of 2005, related legislation against self-referral for standalone imaging centers, the increased scrutiny of third-party insurers in their preauthorization processes, and the reduction in the availability of capital."

But is the slowdown in growth a harbinger of a long-term trend?

"The market for fixed PET imaging units is still relatively early in its adoption cycle, so we're not altogether pessimistic about the longer-term future of the PET and PET/CT market, as over half of the PET sites use a mobile service provider, while about 900 sites own one or more fixed PET or PET/CT scanners," Young said.

A market forecast scenario presented in the report shows that over the next few years, 55% of the PET scanner demand will come from first buyers, such as those who currently use mobile services, whereas 30% will be replacement buyers and 15% will be additional buyers, Young said. In addition, most of the replacement purchases now being made are to replace PET systems with PET/CT, she said.

"PET/CT has become the configuration of choice due to its ability to combine metabolic and anatomical diagnostic information in one image," Young said. "As a result, we are seeing that while 26% of the total fixed units installed are PET scanners and the other 74% are PET/CT scanners, the changeover from PET to PET/CT has been swift."

Looking at annual purchases/installations, 60% of the units installed in 2001 were PET-only systems, a figure that dropped to 3% in 2007 and 0% in 2008. The IMV survey also noted that the future buyers of PET/CT scanners are favoring configurations with 16 or more CT slices.

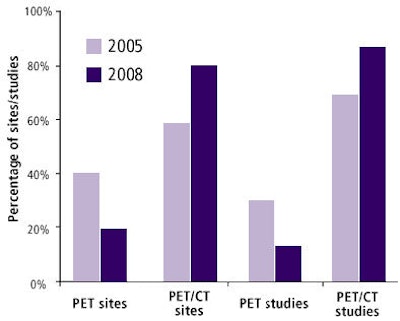

The drop in PET-only system sales is mirrored in the number of studies conducted on PET-only scanners. IMV's study shows a decline in the percentage of studies performed on PET scanners from 30% in 2005 to 13% in 2008, whereas studies performed on PET/CT scanners increased from 69% to 87% in the same three-year period.

|

| PET-only sites/studies versus PET/CT sites/studies, 2005 and 2008. |

Some good news for the future of the PET market is the recent action taken by the U.S. Centers for Medicare and Medicaid Services (CMS), which is planning on expanding PET reimbursement. On January 6, CMS proposed a new coverage methodology that would replace the four-part framework -- covering diagnosis, staging, restaging, and monitoring response to treatment -- with a two-part framework that differentiates the use of FDG-PET imaging in the initial treatment plan from other uses related to guiding subsequent treatment strategies.

Under the new guidelines, CMS would reimburse for one FDG-PET study for patients with solid tumors that are biopsy-proven or "strongly suspected" based on other diagnostic testing, when the patient's treating physician determines that the FDG-PET study is necessary to determine the location and/or extent of the tumor. A final national coverage determination will be issued in April.

One factor that could inhibit the growth of PET/CT scanner purchases is the comparatively low average number of hours of operation for most sites. The 40-hour workweek that most fixed PET and PET/CT systems operate in leaves more capacity to be used before sites would purchase an additional unit.

"On average, fixed PET and PET/CT sites are open for scheduled procedures for 11 fewer hours per week [Monday through Friday] than all CT sites, and 18.5 fewer hours per week than hospitals with fixed MRI," Young said.

Radiopharmaceuticals and procedure growth

According to the IMV study, 97% of PET imaging sites use outside suppliers as their source of radiopharmaceuticals, 2% use a cyclotron onsite, and 1% use both. Of all PET categories in 2008, fixed PET/CT users were the most likely to use a cyclotron onsite. Sites with a cyclotron onsite had the highest average number of patient studies, an average nearly three times that of sites that use outside suppliers.

The percentage of sites with larger radiopharmaceutical budgets is growing: IMV's study shows a 22% increase in the proportion of sites with budgets of $150,000 or more. While all 2008 radiopharmaceutical budgets greater than $50,000 are higher than their 2002 levels, the largest increase is in budgets of $150,000-$249,000, with a steady growth of 12% in the six-year period.

By James Schneider

AuntMinnie.com contributing writer

February 17, 2009

Disclosure notice: AuntMinnie.com is owned by IMV, Ltd.

Related Reading

CT installed base triples in cardiology practices, December 23, 2008

IMV: Nuclear med procedures up in 2007, November 11, 2008

Radiation oncology procedure volume edges up, report states, August 28, 2008

MRI procedure growth rate slows, study shows, June 5, 2008

PET drives growth in nuclear medicine market, April 30, 2008

Copyright © 2009 AuntMinnie.com