The digitization of radiology's last analog frontier -- radiography -- continues its inexorable move forward as a growing number of hospitals across the U.S. are finding that digital x-ray is a good match for their balance sheets, populations, and most common clinical applications.

Shipments of digital x-ray systems -- encompassing computed radiography (CR) and digital radiography (DR) -- have grown rapidly in recent years. Even DR, which experienced a rocky start when first launched in the late 1990s, is in the midst of a major growth spurt, and fully 50% of x-ray systems shipped in 2005 in the U.S. were DR units, according to the new "2005/2006 X-ray/DR/CR Market Summary Report" by IMV Medical Information Division of Des Plaines, IL.

The report explores the digital x-ray terrain of 1,500 U.S. hospitals, with results projected to the 4,860 hospitals performing general x-ray procedures in the U.S. It finds that:

- There is an average of 3.4 general x-ray devices installed in any given hospital's radiology department.

- 62% of these hospital sites have some combination of analog x-ray, computed radiography (CR), and digital radiography (DR).

- 38% of hospitals have only analog x-ray.

For many reasons, not the least of which is clinicians' comfort levels in adjusting to new technology, x-ray has been one of the last digital frontiers. Just as some people will always prefer pictures taken with film cameras to digital snapshots, many radiologists prefer analog x-ray to digital and are wary of digital x-ray's image quality and expense.

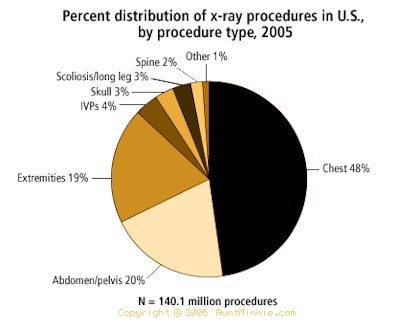

|

The sheer volume of general x-ray procedures performed in the U.S. makes going digital a logistical challenge: An estimated 140.1 million exams were done in U.S. hospitals in 2005, according to IMV data, with the average number of total procedures per hospital totaling 28,815.

But with a current installed base of more than 16,500 x-ray imaging systems -- including conventional and DR units -- at 4,860 U.S. hospital sites, and with the overall momentum toward digital occurring across hospital departments, digital x-ray's time seems to have come. In fact, IMV's report found that 30% of these sites have at least one DR system in their x-ray department, and 56% have installed CR technology. In 2006, 71% of imaging acquisition units purchased are expected to be DR, while 29% will be conventional x-ray (either CR or analog).

|

CR or DR?

A facility's decision about whether to upgrade analog devices to digital with CR cassettes and readers, or to replace analog rooms with DR systems, is influenced by how many x-ray systems a hospital currently has and its procedure volume. The more x-ray rooms a hospital has, the more challenging it is to find the funds to replace them all with DR technology.

DR's cost remains a key factor in whether to convert to digital, although its price has dropped by at least 20% in the last few years. DR system prices range from $225,000 to more than $500,000; a single-plate DR room might cost $300,000, while upgrading an analog room with a CR unit can be almost half as much, at about $170,000.

In this case, CR is cost-effective and doesn't require a lot of staff training: With a cassette retrofit and one CR reader, many rooms can be digitized at once. CR is a sturdy option for facilities that use portable x-ray. Jarring or even dropping a DR detector is not only costly but also detrimental to patient care. Some clinicians believe that CR is the better technology for certain axillary views of the shoulders, as well as for ER applications. Finally, if a CR unit breaks and the room has to be shut down, the x-ray acquisition device can still be used with film.

But DR does have compelling benefits, particularly with regard to productivity. With images being sent directly to a display, there's almost none of the processing time required by film-screen x-ray and CR. The larger a hospital is, the more DR makes sense.

Nearly 59% of the hospitals with 400 or more beds that participated in the IMV survey have at least one DR unit, while only 15% of hospitals with 100 beds or fewer did. In addition, the installed base of DR systems is fairly new: 90% of installed DR systems were purchased in 2000 or later, with the median purchase year being 2004.

Finally, going digital has become a corporate strategy at many facilities. The advent of PACS has given integrated delivery networks (IDNs), regional healthcare systems, and multihospital systems leverage in the radiology marketplace and has motivated hospital networks to make the quick delivery of clinical data available to their referring physicians across departments and locations.

What is the future of digital x-ray? Growth will be driven by the replacement of the installed base of aging conventional radiography systems, according to the report's data: the survey estimates that 85% of future purchases will be replacement systems, while 15% will be additional units.

By Lorna Young

AuntMinnie.com contributing writer

October 12, 2006

Lorna Young is senior director, market research at IMV Medical Information Division and is the author of IMV's "2005/2006 X-ray/DR/CR Census Database." For further details and information, visit IMV's Web site at www.imvlimited.com or call 847-297-1404.

Related Reading

Digital radiography slowly, but surely, makes its mark, July 25, 2006

Digital x-ray unreliable for evaluating bone healing, May 31, 2006

Asian digital x-ray market primed for growth, February 17, 2006

PACS drives European CR, DR market, January 10, 2006

Copyright © 2006 AuntMinnie.com

Disclosure notice: AuntMinnie.com is owned by IMV, Ltd.